NVIDIA is committing £2 billion to AI startups from Oxford and across the UK.[1] When Jensen Huang, NVIDIA's founder, stood alongside Prime Minister Keir Starmer in September 2025, he framed it as a historic moment:

“This is the age of AI — the big bang of a new industrial revolution.”

Huang described “the largest AI infrastructure investment the UK has ever seen”, including new supercomputing capacity and expanded support for British startups. For Oxford, and the UK more broadly, this announcement was both a rallying cry and a reminder of how much is at stake.

And it's not just NVIDIA. Larry Ellison, Oracle's billionaire founder, is also betting big on Oxford.[3] Through the Ellison Institute of Technology (EIT), he has committed over £100 million to joint research, infrastructure, and scholarships, is building a billion-pound Oxford campus by 2027, and has already launched a £118 million AI-vaccine initiative with Oxford's Vaccine Group. Ellison has even taken a significant stake in Oxford Nanopore, one of the university's most high-profile spinouts. The news of EIT's planned £10bn investment over the next ten years into Oxford was applauded by the Chancellor of the Exchequer, Rachel Reeves, and Oxford's Vice-Chancellor, Professor Irene Tracey.

These headline-grabbing moves signal something larger: Oxford is no longer just a historic university town. It's one of the front lines in the next industrial revolution.

Oxford's Engine in Motion

Despite successes like DeepMind, Isomorphic Labs, and Helsing, scaling world-class AI companies in the UK has been notoriously hard, with limited compute, patchy venture capital outside London, rising energy costs, and uneven support for founders spinning out of universities like Oxford.

Yet Oxford's own numbers show its innovation engine is firing. According to Oxford University Innovation (OUI),[4] between August 2023 and July 2024 the university raised £19.5m in seed funding and £872m in follow-on investment, launched 15 new companies (10 spinouts, two social ventures, three startups), filed 93 patents, and struck a record 1,239 licensing deals across sectors from HealthTech to clean energy.

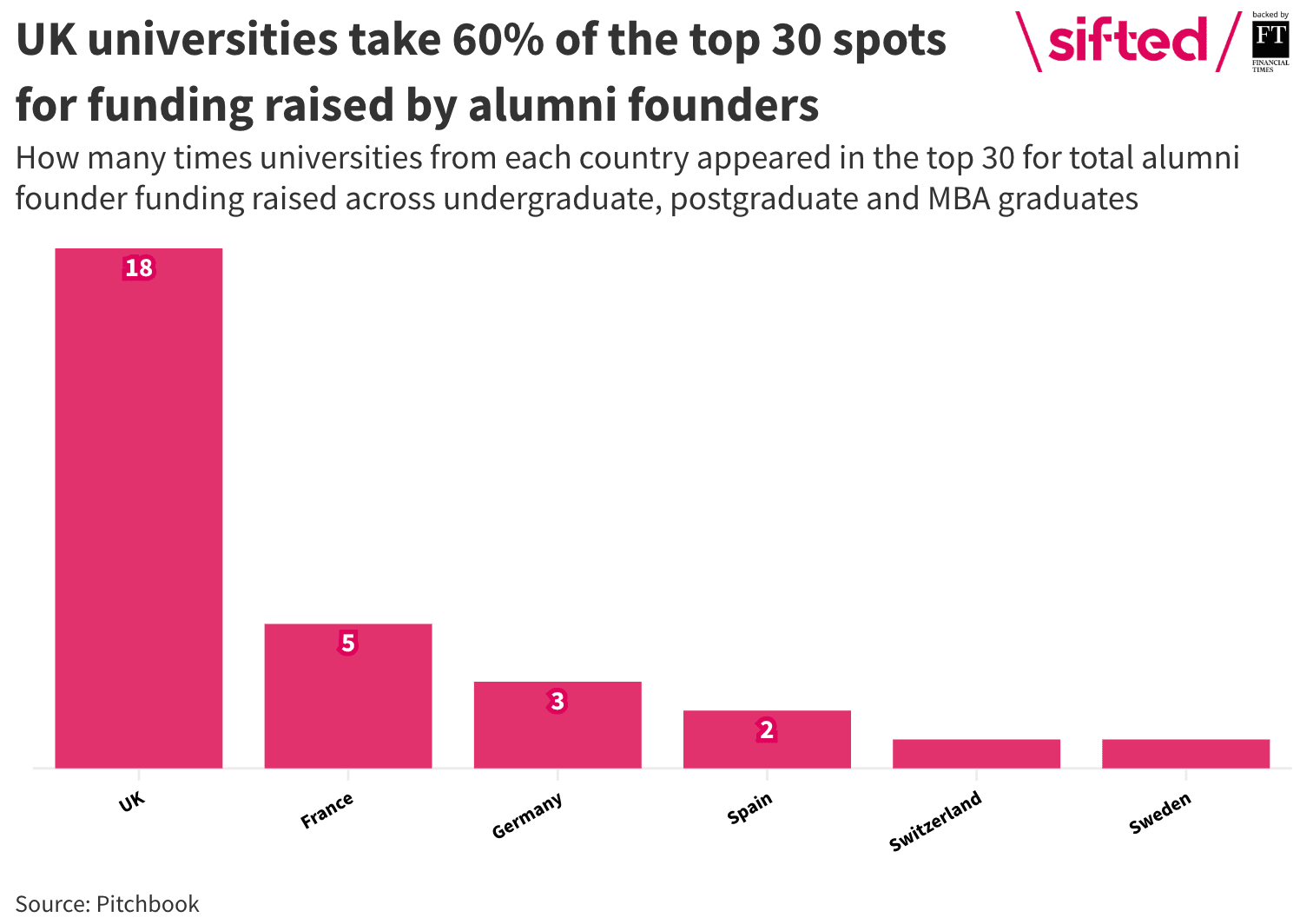

The story doesn't stop at Oxford's gates. PitchBook ranked Oxford the #1 European university for raising VC among undergraduate alumni founders[5], think Monzo's Tom Blomfield or Onfido's Hussayn Kassai. Postgraduate alumni kept Oxford on top again, raising $29.9 billion in 2023, edging past Cambridge's $29.3 billion. Globally, Oxford sits 8th for producing startup founders, just behind Cambridge (7th), the only two non-US universities in the top 10.

Patents, Spinouts, and Startups

The IP story is equally striking. A study by the German Economic Institute[6] ranks Oxford the highest non-US university (7th worldwide) for international patent filings. Licensing revenues tell a similar story: £145m in 2023, supercharged by the AstraZeneca COVID-19 vaccine license.

In deep tech, Oxford continues to dominate. According to the Royal Academy of Engineering's Spotlight on Spinouts 2025,[7] Oxford leads the UK with 225 spinouts as of January 2025, ahead of Cambridge (175) and Imperial (132). Together, the Golden Triangle (Oxford, Cambridge, London) accounts for 27.7% of all UK spinouts.

Startups show the same pattern. PitchBook reports that UK universities make up 80% of the top 10 institutions for undergraduate alumni founders in Europe.[8] Oxford undergraduates lead with 286 founders, while Cambridge edges ahead at the graduate level. Yet Oxford still claims a strong second, with 981 postgraduate alumni founders recorded through 2023.

The Oxford Paradox

But here's the twist.

Over coffee a few years back, a founder sighed: “Oxford is both the best place and the hardest place to build a company.”

Her frustration is backed by data. Research by Oxford academics[9](Hellmann, Mulla & Qian, 2025) shows the university has trimmed its equity stake in spinouts from roughly 47% in 2010 to roughly 17% in 2021 (close to the Spotlight Report's 20.8% average). Yet it still takes nearly twice as much as Cambridge (10.8%).

That gap reflects deeper differences in IP policy. Oxford claims ownership of most staff and student IP under its Statutes. Cambridge allows researchers to opt out, and students generally keep their IP unless tied to employment or specific funding.

The implications for founders are twofold. First, dilution: a 20%-plus university stake means less equity left for the people building the company. Second, investor concerns: VCs worry about “founder incentive misalignment.” Every 1% increase in university stake reduces the chance of raising VC by 0.8–0.9%, and spinout formation by 0.6–0.8%.

On the one hand, Oxford's brand is a magnet, with investors trusting the pipeline of ideas. On the other, the very structure of its deals risks slowing down company creation. By contrast, Cambridge looks more like the big US powerhouses. Universities like MIT (roughly 5%) and Stanford (low single digits) take only a sliver, aligning incentives for both founders and investors. It's hard not to wonder how many more companies might come out of Oxford if its equity model looked more like MIT's.

Capital Firepower

Oxford has leaned heavily on Oxford Science Enterprises (OSE), which helped lift spinout activity from just 4–5 a year to 15. But questions remain: does Oxford have enough firepower to compete globally?

Cambridge launched Cambridge Innovation Capital (CIC), a £50m fund designed to back IP and founders with a hybrid model that blends returns with ecosystem building. Oxford has no equivalent.

The need is pressing. In a submission to the UK Parliament's Science and Technology Committee (January 2025), Oxford estimated its spinouts will require £2–5 billion over the next five years, particularly in capital-intensive fields like quantum, climate mitigation, and late-stage scale-ups.

AI as the New Industrial Revolution

But capital alone isn't the story.

At the centre of this transition are the founders themselves, the scientists-turned-entrepreneurs, the postdocs coding AI models at 2 a.m., the clinicians pushing biotech out of labs and into trials.

Ever since the release of ChatGPT in late 2022, the innovation landscape has been rewritten. What was once a slow, technical march of AI research suddenly leapt into public consciousness. For universities, startups, and investors, it unlocked dizzying possibilities but also thorny challenges: new markets opening overnight, fierce competition, ethical dilemmas, and an arms race for talent and compute.

Whether we fancy it or not, AI now underpins everything from finance to health to national security. Europe excels in deep-tech research (2025 European Deep Tech Report[10]), but it lags the global AI race. The US and China lead with unified markets, capital, national AI strategies, and massive GPU clusters. AI has become the connective tissue across deep-tech, accelerating drug discovery, reshaping climate modelling, supercharging materials research. Europe's limited access to infrastructure and capital only widens the perceived innovation gap.

Oxford sits right at this fault line. Its 225 spinouts are part of Europe's attempt to anchor the deep-tech transition in an AI-driven era.

The Billion-Pound Question

Collaboration becomes ever more important in Oxford's innovation ecosystem. Founders may carry the torch, but their success depends on a whole constellation of allies, including mentors, investors, policymakers, and peers. The question isn't just how many spinouts Oxford can produce, but whether the community and ecosystem around them can give founders the lift to compete globally.

This means tighter links between labs, capital, and market, but also bridges outward, to London VCs, European partners, US and Asian markets, and policymakers shaping the rules of AI.

And this brings us back to NVIDIA and Larry Ellison. Their billions directly address Oxford's biggest pain points: compute, infrastructure, and early-stage capital. Yet their investment doesn't erase the deeper structural challenges, including high equity stakes, fragmented markets, and the absence of scale-up funding.

If Oxford is to anchor Europe's role in the new innovation era, an era reshaped daily by advances in AI, shifting geopolitics, and technological upheaval, it cannot go it alone.

Sources

- [1]Business Chief. (2025, November 12). UK AI investment behind NVIDIA's pledge into AI startups. Link

- [2]NVIDIA. (2025, November 11). NVIDIA announces $2 billion investment in the United Kingdom AI startup ecosystem. Link

- [3]The Times. (2025, November 11). Larry Ellison to invest extra £890m in Oxford institute. Link

- [4]University of Oxford. (2024, November 15). Oxford University Innovation's 2024 Impact Report showcases a year of transformative innovation. Link

- [5]Sifted. (2024, December 5). Europe's top universities by founder alumni and startup funding. Link

- [6]Haag, M., Kohlisch, E., & Köppel, O. (2024). International ranking by country and individual university. Institut der deutschen Wirtschaft Köln. Link

- [7]Royal Academy of Engineering. (2025, March). Spotlight on Spinouts 2025. Link

- [8]Sifted. (2024, December 5). Europe's top universities by founder alumni and startup funding. Link

- [9]Hellmann, Mulla & Qian. (2025). University equity stakes and spinout formation. SSRN Electronic Journal. Link

- [10]Dealroom & Lakestar. (2024, November). 2025 European Deep Tech Report. Link